There's nothing like the annual ritual of Wall Street's gaze into the cloudy crystal ball...

Every December, the big banks roll out their polished S&P 500 forecasts for the year ahead. For the past few years, I've been tracking the forecasts of UBS, Goldman Sachs, Morgan Stanley, Bank of America, & JP Morgan Chase, and the results are laughable. The moral of the story: no one knows what the market will do next, and relying on these forecasts as any semblance of a "guide" is foolish.

Before we prepare for 2026, here's a visual trip down memory lane. As you look at these charts, remember that these banks employ the world's brightest financial minds, including highly-decorated Ivy League graduates, and a seemingly endless budget for research & technology:

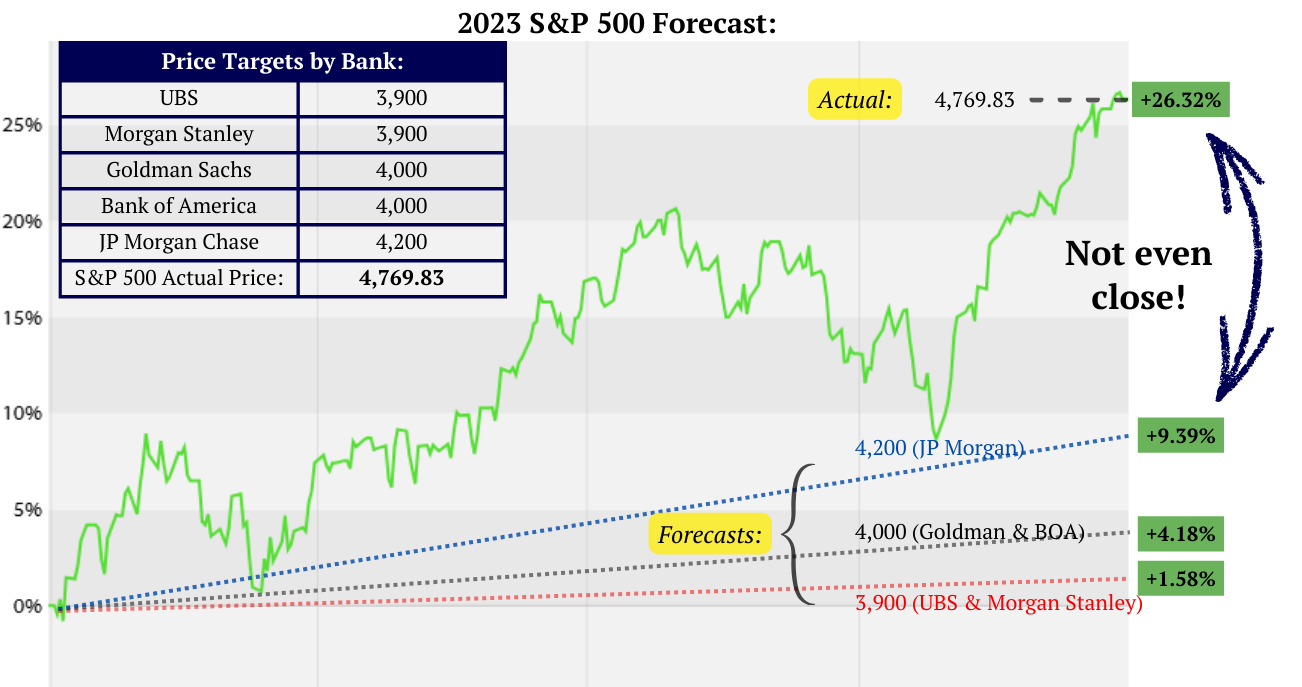

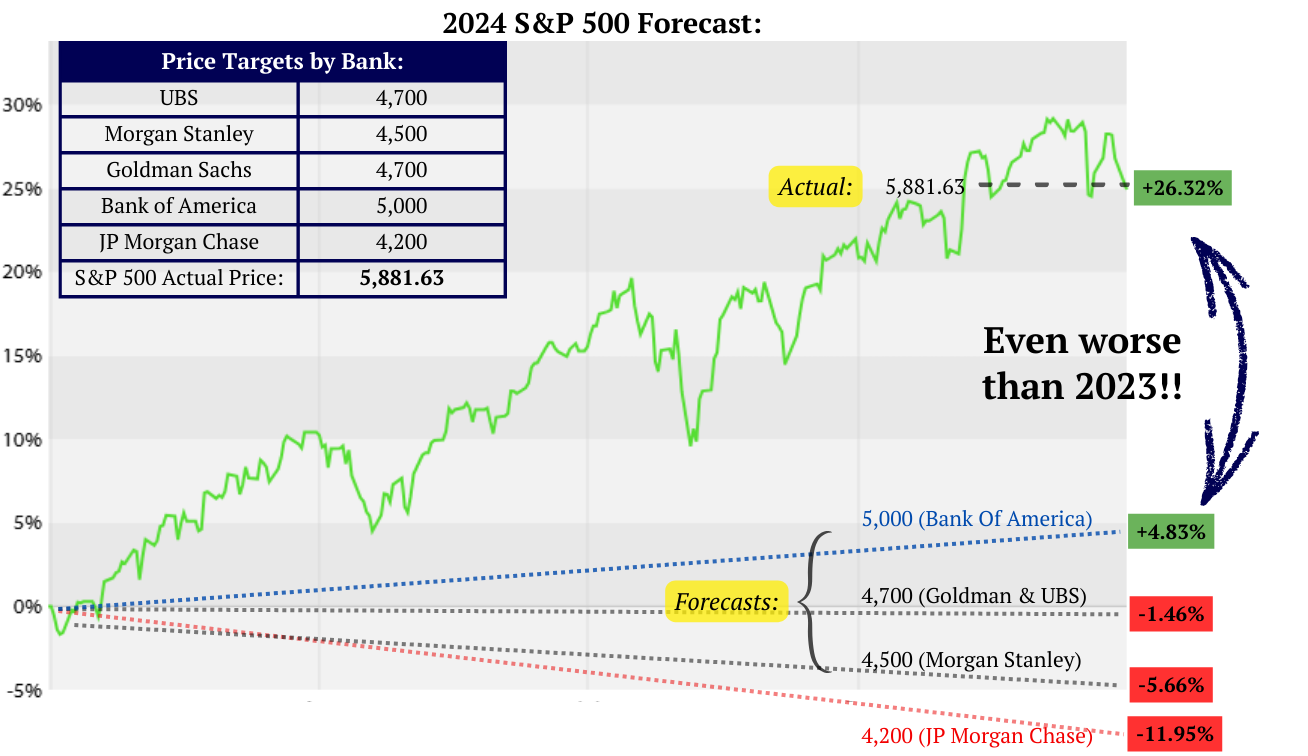

Here are the market returns compared to the "Big Banks" forecasts for 2023 -2025:

The "best guess" out of this group still underestimated the market by more than 16%...

Couldn't hit water if they fell out of a boat! JP Morgan Chase, arguably the most well-known investment bank on the planet, predicted nearly a 12% drop in a year where the market climbed by 26%. Yikes...

That's better...after a few years of significant market performance, the banks decided to get on board. And 2025 encapsulated the emotional life of a successful investor: the tariffs created a white-knuckle Q1, during which I urged my clients to trust the process. The markets rebounded by 30%+ from the bottom , and we're all wealthier because of our patience. Welcome to investing, rinse and repeat.

My advice comes from a place of long-term thinking, so don't expect some ultra-specific "price targeting" that is sure to be wrong. I'm not dumb enough to think I can guess what stocks will do in the next 12 months. But, I'll give you some historical context to frame 2026. Philosophically, I subscribe to evidence-based research, meaning I'll use market history to help better understand today's investing environment.

Stocks generally go up: Over the last 10 years, stocks have risen 8 times. Over the last 20 years, they have risen 17 times. So think of investing like planning a beach vacation; the weather will generally be sunny, and a 20% chance of rain here or there shouldn't force you to cancel the trip...

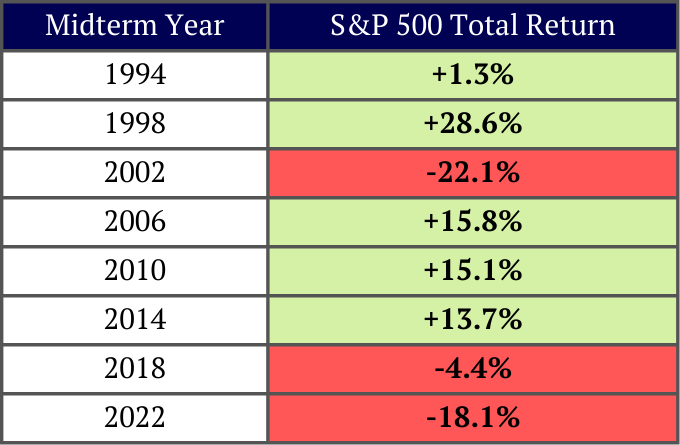

I broke down the 4 years that make up a presidential cycle, and compared the results. To have the same sampling size of each, I went back to 1994, giving us 8 instances of each "type" of year:

History shows that midterm election years tend to be weaker than normal, but still generally positive (up 63% of the time since 1994). So to continue with the vacation analogy, don't be surprised if 2026 has some extended periods of cloudiness, but hopefully still more sunshine than rain.

Below are the annual returns of the previous 8 "midterm years". Four were really strong, 2 sideways years, and two were ugly. Here's to hoping that 2026 lands on the positive side of the ledger.

As an investor, the best strategy is the one you are able to stick with, no matter if markets are moving up or down. Making changes based on forecasts is a recipe for heartburn. To reduce your financial stress, strive to make your investment decisions based upon the next 10 years instead of the next 10 months.

As a seasoned advisor, I've found those who are willing to plan tend to focus on the big picture versus the year-to-year market moves. With today's technology, it's never been easier to get your financial plan off the ground. While financial planning won't answer all of your questions, it will at least get you headed down the right path. Getting a handle on your own personal cashflow, tax rate, & investments will help you better understand how your future may ultimately unfold.

Ready to Get Started? Click here to learn more about our One Page Plan.

Important Disclaimer: The information provided in this guide is for educational purposes only. All examples used are based upon a fictitious client that resembles our typical clients. Nothing here within should be considered investment or tax advice. Please consult with a financial advisor and/or CPA when considering investment and tax decisions.

We generally serve families with $500k or more in retirement/investment assets. Our clients are seeking a trusted advisor to oversee investment decisions and retirement planning. Schedule a meeting to explore our services:

Schedule a Call

.png)