.png)

Recessions, geopolitical tensions, pandemics, elections, policy shifts....bad news happens, and stocks feel the impact. As investors, we've seen it all: the COVID crash of 2020, the inflation-triggered disaster of 2022, and last year's tariff volatility that shaved nearly 19% off the S&P 500 before rebounding to new highs.

Yet, history shows that surviving these downturns is key to unlocking the market's long-term gains. Reward doesn't come without risk. With the right mindset and tools, you can survive the next market drop & potentially emerge stronger. In this guide, we'll define & review bear markets, explain some battle-tested strategies, and help you reflect on your own experiences. Let's turn market fear into your competitive edge.

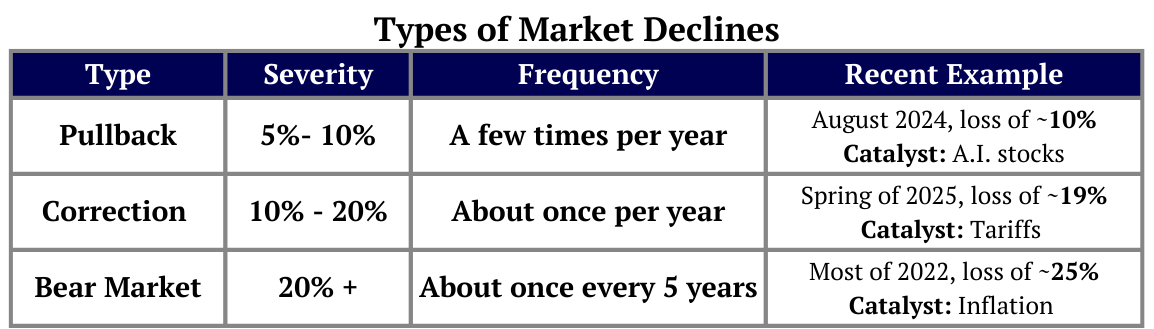

Stock drops aren't created equally. Here's a simple breakdown to explain the differneces:

Are Declines Annoying? Yes. Inevitable? Absolutely. But history shows they are temporary blips on a gradual upward trajectory. In hindsight, every previous decline was actually a great buying opportunity.

Yes! In fact, stocks spend far more time advancing versus declining, yet the downturns garner most of the attention. Bad news sells...Consider these statistics:

The hard part: to experience the "good", you must also take the "bad". Its impossible to guess when the market will fall; choosing to accept this reality will improve your investing experience.

Market drops are normal. Like a common cold, they're frequent, but fleeting. And every so often your cold turns into the flu, which takes a little longer to recover from. These moves are considered normal market behavior. Use 2025 as proof: we survived a significant Q1 correction (-19%) & recovered to new all-time highs before year end.

Action Step: Get used to tracking your investments quarterly as opposed to daily. When stocks are failing and you're losing money, incessantly checking your balance won't fix the issue. It may actually lead to an emotionally-charged decision to sell your stocks, which is the worst thing an investor can do!

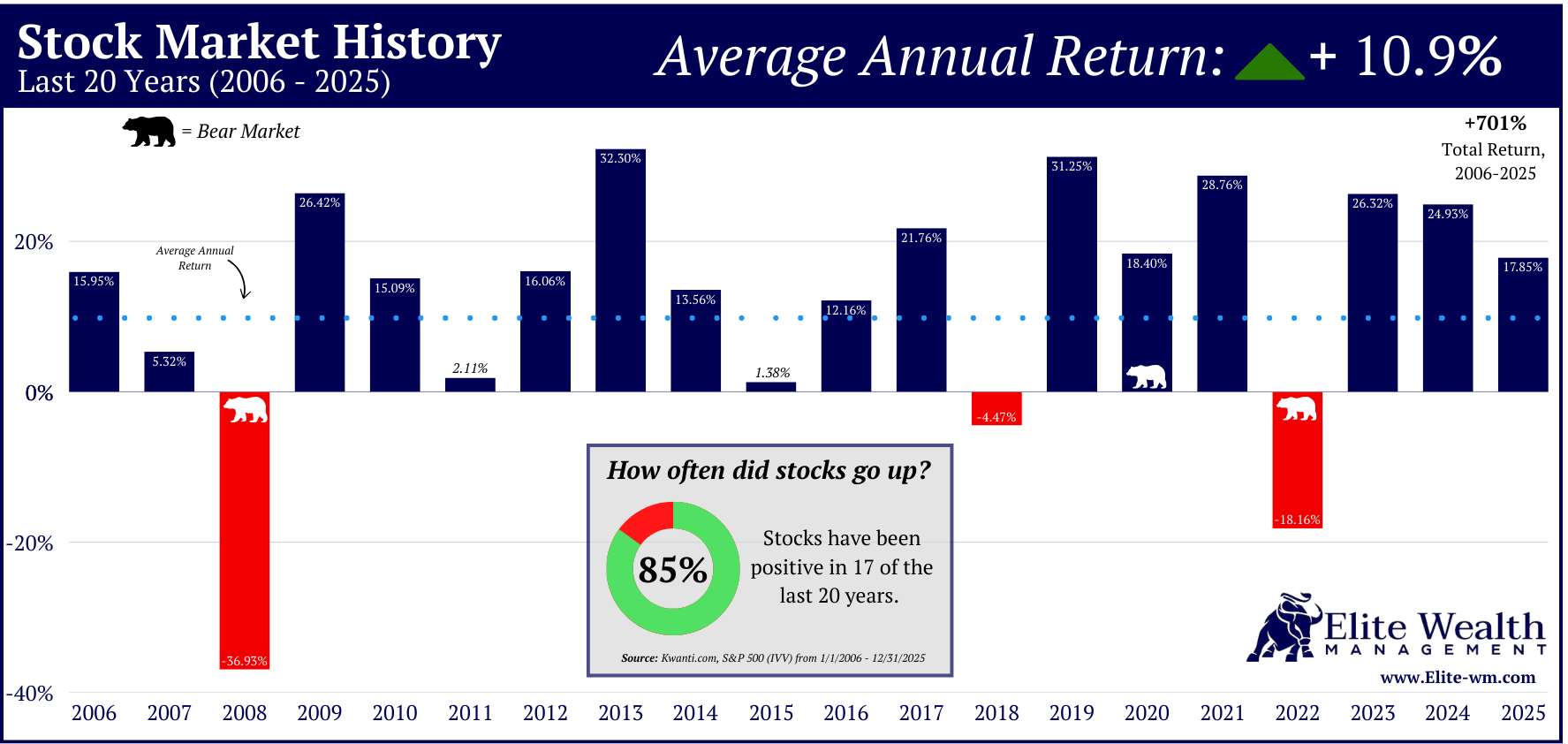

The media loves to compare the stock market to a casino, where fortunes can vanish on a single bad roll. Sure, drops are part of the program—but that doesn't make holding stocks a loser's bet. Stock investing is a proven wealth creation tool that anyone can access. Just look at the numbers: From 2006 to 2025, the S&P 500 posted positive annual returns in 17 out of 20 years, averaging nealy 11% per year. If roulette or blackjack paid like that, Sin City would be a ghost town. This isn't a 50/50 crapshoot—it's an asymmetric growth opportunity for those who invest for the long term.

Action Step: Review the historical returns of your current positions with an advisor or through tools like Morningstar & Yahoo Finance. Compare the returns to the market indicies to see how your strategy stacks up and look for any areas of weakness.

How much stock do you own? When are you retiring? Do you need income from your investments? Investing is not a one-size-fits-all proposition.

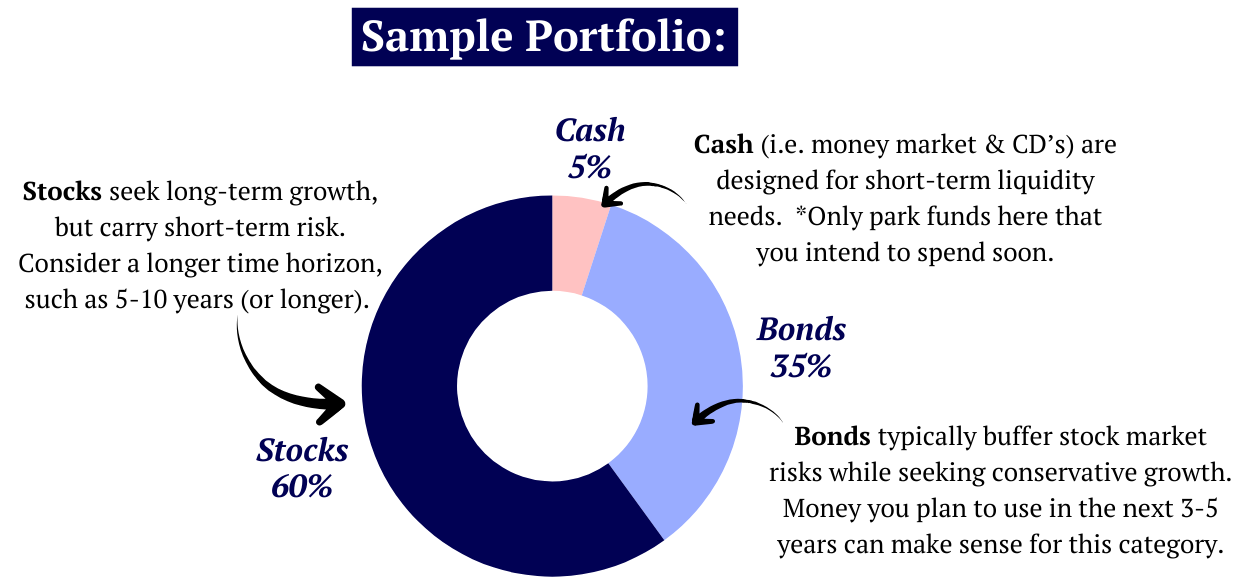

Proper investing utilizes diversification across various investment vehicles based upon your very unique circumstances. For example, a 45 year-old might hold 80% stocks whereas a 65 year-old may hold 40% stocks. Working with an advisor can go a long way towards fine-tuning your portfolio mixture.

Know the Basics: What do you own?

What's the best investment strategy? The best strategy is the one you can stick with during both good and bad markets. Of course, ongoing adjustments are necessary as life progresses.

Action Step: Work with an advisor to help identify your blind spots. Spend time understanding the risks within your own portfolio. Determining your investment strategy should be based upon your objectives and backed by research, not your gut feelings. Do you want my opinion on your portfolio? Click here to get started.

I'll save you some time...the headlines will read "Stocks Get Crushed", "Imminent Market Crash", or "Markets in Turmoil". Clickbait at its finest...

Even your "rich neighbor" will tell you, "Trust me, this time, it's different..."

Spoiler Alert: This time is not different. While human panic is eternal, rebounds are reliable. It's been this way for 100 years. Panic selling will make you feel better for a few days, but the collateral damage may cost you a few years.

Another popular excuse: "I'm getting out of stocks until things calm down"; I've heard this a thousand times. This is arguably the most dangerous phrase in investing. There will never be an all clear signal to let you know its safe to get back in the market...odds are you will be forced to buy back in at higher prices.

Action Step: Watch less news, limit your doom-scrolling, and avoid the rabbit holes. Unfortunately, social media is a great amplifier. If you're looking for any assurances that things will improve, you won't find it here. Trust the process, remember the historical data from above, get outside, spend time with friends...

Over time, your strategy will shift purely based upon "market drift". If left alone, a conservative portfolio can creep towards an aggressive one. Rebalance at least annually to your target asset mix. But, be mindful of taxes! Tax-deferred accounts can rebalance freely, whereas after-tax accounts may trigger taxable events.

Think of rebalancing as the forced act of selling high and buying low...you're most likely selling positions that have grown and using the proceeds to buy positions that haven't performed as well.

Action Step: Determine your desired portfolio mixture; for example 60% stocks, 35% bonds, & 5% cash. Then, pre-determine when you will rebalance, such as quarterly or annually. Stick to the script; regardless of current market events, rebalance as planned. *Its strongly advised to work with an advisor to properly create a rebalancing plan.

Think back to 2020, 2022, & the spring of 2025; all were painful periods for stock investors. Consider these questions:

No matter how stressed you felt during these events, the ensuing rebounds clearly proved that staying invested was by far the best course of action. Panic-selling may alleviate the pain for a week or two, but the long-term consequences can be devasting.

To be a successful stock investor, you must allow contradicting statements to be true at the same time:

The hard part: no one can tell you when stocks will get clobbered next, so simply accepting that it will eventually happen on the path to higher levels is critical. Experience is the ultimate teacher, and the most obvious outcome often doesn't occur. Every down market an investor experiences helps prepare them for the next one!

Important Disclaimer: Investing carries risk, past performance is not indicative of future results. All data pertaining to the "Stock Market" refers to the S&P 500, including any historical returns presented. The information provided in this guide is for educational purposes only. Any portfolio examples used are based upon a fictitious client that may resemble our typical clients. Nothing here within should be considered investment or tax advice. Please consult with a financial advisor and/or CPA when considering investment and tax decisions.

We generally serve families with $500k or more in retirement/investment assets. Our clients are seeking a trusted advisor to oversee investment decisions and retirement planning. Schedule a meeting to explore our services:

Schedule a Call

.png)