Financial planning is an art, not a chore—yet 64% of Americans skip it, thinking it’s too complex or only for the ultra-wealthy. The truth? A simple plan can paint a beautiful picture of your future, and it’s easier than you think. According to a recent study, only 36%* of American adults have a financial plan in place. Let’s explore how to craft yours with clarity and confidence.

I've been an Investment Advisor for nearly two decades, and financial plans for me are the equivalent of a canvas to an artist; it's very difficult to do my job well without the use of financial plans.

My method of financial planning prioritizes simplicity. It's a living, breathing, financial plan designed to guide clients to and through retirement. It creates an organized way to manage your money, leading with education. My digital plans are clear, concise, and easy to update as your life evolves.

If you're curious about financial planning, this guide will show you what we uncover for our clients. Here are steps I follow when building a plan: Asset Organization-> Cashflow-> Tax Planning-> Expenses-> Results.

The typical client has a complex financial life. The primary goal of my planning is to inject simplicity in all areas. I start with asset location and organization, helping the client visualize what they have, where it is, and how it will be taxed. We create a household balance sheet that includes:

Here’s an example of a Household Balance Sheet:

The balance sheet allows me to get eyes on the big picture and identify potential problems as well as opportunities to simplify.

Consolidation: We typically discover that the traditional investor is scattered. It’s common to find multiple accounts that can easily be consolidated into an existing account, making the seemingly-endless stream of account statements significantly less. This is also the easiest way to get your estate planning organized, which is frequently overlooked. It's surprising to see how many accounts investors acquire over the years with jobs changes, inheritance, and other circumstances.

Identifying your income sources helps determine how much you can afford to spend and what your overall tax picture may look like.

Pre-Retirement: For those who are still working, cashflow planning can shape a proper savings plan, focused on automation as well as tax-efficiency. We provide guidance on how to handle items such as:

Here's an example of our Cashflow Analysis:

For those who are retired, the process is the same. We identify all expected income sources (such as social security & pensions) to properly create the most tax-efficient portfolio distribution strategy, seeking to cover ongoing expenses.

What you make is far different than what you keep. Once we have outlined the income sources, we can calculate the expected tax liability. Using the same example from above, here’s an estimated view of how John & Sue’s income of $408,500 would be taxed:

As the example shows, we immediately look for ways to reduce taxable income while improving your savings strategy. Determining taxable income allows us to customize your savings or distributions to optimize for tax-efficiency.

This is where many plans experience a major disconnect. Simply put, many investors don’t know how much they spend, and they don't care to "track a budget". To help solve this problem, we work with clients to reverse-engineer their budgets, along with building “target spending ranges” based upon what their plan can withstand. Here’s an example:

“Am I going to be ok?” This is the question that investors seek to answer as they work through a financial plan. To help answer this question, we use a Monte Carlo Analysis to determine if our clients are on track. The analysis is designed to model the uncertainty and variability of future outcomes by running 1,000 simulations of the plan, producing a probability of success score (or lack thereof).

While the Monte Carlo Analysis isn't perfect, it’s a great starting point to help identify potential issues that are present with a client’s current financial picture.

What if....One thing we know is that the original plan won't play out perfectly. To combat this, we provide details on many "what if" scenarios to see how your plan would hold up, such as:

By modeling various "what if's" along with updating our client plans every 6 months, we strive to create a level of financial comfort that otherwise wouldn't exist. As a result, we frequently see clients becoming more comfortable with short-term market moves as their focus shifts towards the big-picture planning.

As an advisors who's built hundreds of plans, the biggest hurdle for most is simply getting started. With today's technology, it's never been easier to get your plan off the ground. While financial planning won't answer all of your questions, it will at least get you headed down the right path. Getting a handle on your own personal cashflow, tax rate, & investments will help you better understand how your future may ultimately unfold.

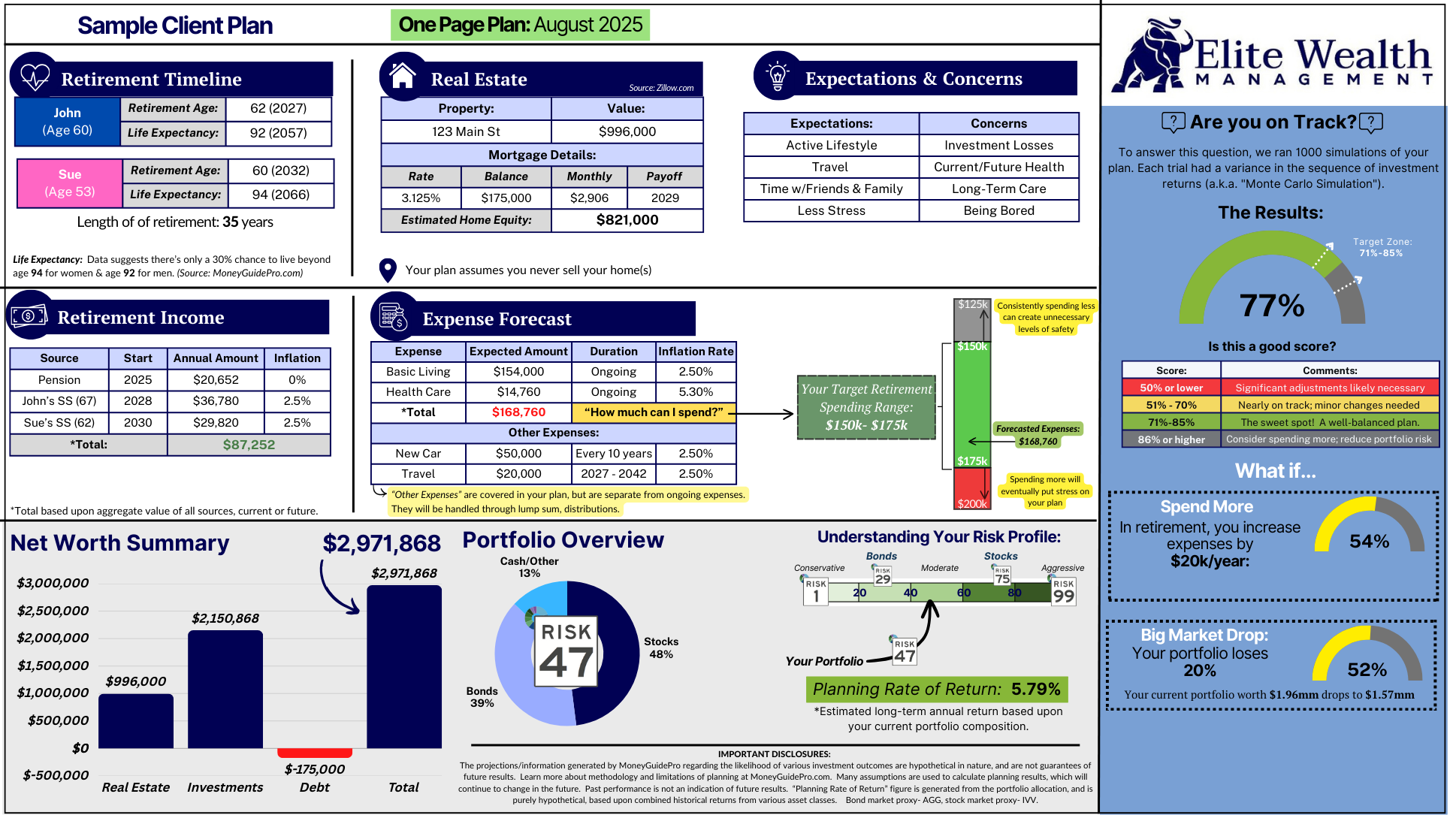

Ready to Get Started? Here's a sample of our One Page Plan:

Important Disclaimer: The information provided in this guide is for educational purposes only. All examples used are based upon a fictitious client that resembles our typical clients. Nothing here within should be considered investment or tax advice. Please consult with a financial advisor and/or CPA when considering investment and tax decisions. *The 36% figure for U.S. households or adults with a long-term financial plan is drawn from the 2024 Northwestern Mutual Planning & Progress Study (published April 2024), which surveyed over 2,000 Americans. This is consistent with prior years' data from the same annual study, showing little change into early 2025.

We generally serve families with $500k or more in retirement/investment assets. Our clients are seeking a trusted advisor to oversee investment decisions and retirement planning. Schedule a meeting to explore our services:

Schedule a Call

.png)