The idea of retirement tends to trigger a wide range of emotions...exciting, but at the same time, full of unknowns. Answering the big question of, "When can I retire?" depends upon an array of factors that are constantly in flux. While everyone's situation is unique, there are a few key factors that will certainly impact your retirement date. Let's explore.

Before we dig into your retirement roadmap, understand that this is what we do: At Elite Wealth, we've made a career out of turning "someday" into "today" for clients just like you. Picture this—over half of our clients are already enjoying retirement, whether its travelling the world or taking it slow. Some are chasing grandkids while others are chasing golf balls. And for me, retirement is when the work truly begins, steering retirees through market twists and life changes.

At the most basic level, its starts with answering these 4 questions:

From a planner's perspective, its always better to over-estimate this one. A solid retiremnet plan needs some margin for error. For example, if your plan can support your lifestyle to age 92, and you pass away at 88, there's some money left for your heirs. Conversely, if you plan to live until age 88, but actually live to 92...then we've got a problem!

How Long Are Americans Living? According to the latest CDC data (2023), the average mortality age is 78.4 years old. For men, it's closer to 75 and for women, age 81. But no one wants to be average! Account for additional longevity in your planning.

Our plans assume that men will live to age 92 and women to age 94. Based upon data from our planning software (MoneyGuidePro), there’s only a 30% chance to live beyond those ages. So that's our starting point; adding more than decade of life to the statistical norms. If your family tree has longevity or lack thereof, then we may adjust accordingly.

Some common sources of retirement income are social security, pensions, and part-time work. In most cases, pensions are fully taxable, as is any employment income. In my experience, social security creates confusion.

Social Security: On average, Social Security replaces about 40% of your working income. When to take your social security benefits is another decision that will impact your ability to retire. Also, make sure you consider taxes when you're calculating your benefit. Check your estimated benefits (www.SSA.gov). Delaying until age 70 can boost payments by up to 8% per year.

.png)

Deciding when to take social security is an important component of retirement planning. We help clients weigh their options based upon retirement age, other income sources, and after-tax assets. For those who can delay taking social security, the increased benefit often improves their overall retirement picture.

Spoiler Alert: You're likely not going to be spending less in retirement than you are now. It's best to assume you'll maintain your current lifestyle, and remember to account for ongoing inflation.

And let's be real, budgeting is painful. Most people don't have the time or energy to crunch the numbers. But, if you hope to retire with confidence, having a rough estimate of what you spend is a critical.

Reverse-engineer your budget: Start with your monthly take home pay (after withholdings & deductions); for example $10k/month. Now, check your last few bank statements- does the $10k cover your needs? This will at least point you in the right direction. Track your inflows versus outflows for a few months to make sure you're at least in the ballpark.

What about big-ticket items? Weddings, vacations, college funds, new cars...don't forget to account for these in your planning.

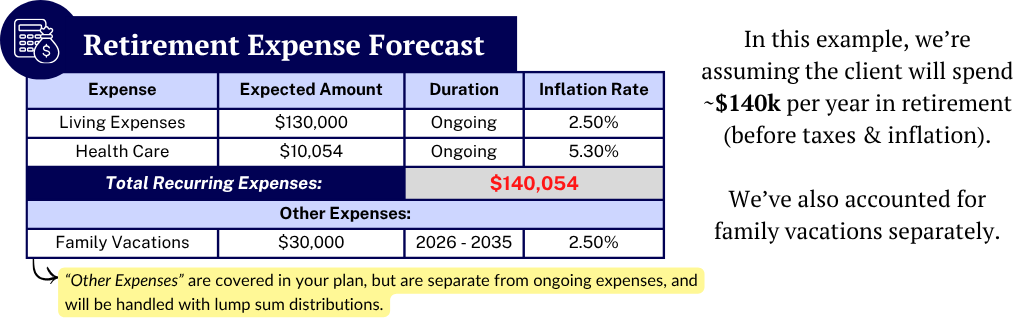

This tends to be where many plans run into trouble. Again, the concept of budgeting and managing expenses is cringy. So we start with an expected expenses forecast:

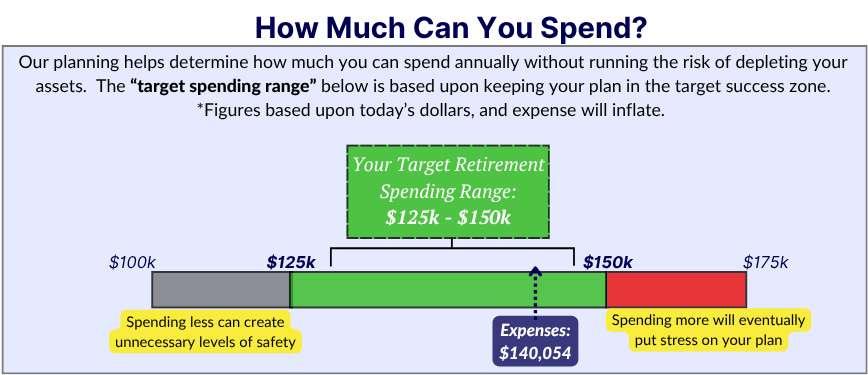

Knowing that expenses will fluctuate, we develop a "target spending range" to show clients what their plan can likely support:

Saying goodbye to your paycheck is hard. Your retirement income sources will likely be less than what you're used to earning, so your retirement savings becomes the lynchpin of your plan. Filling the income gaps with portfolio distributions is a common challenge that retirees face.

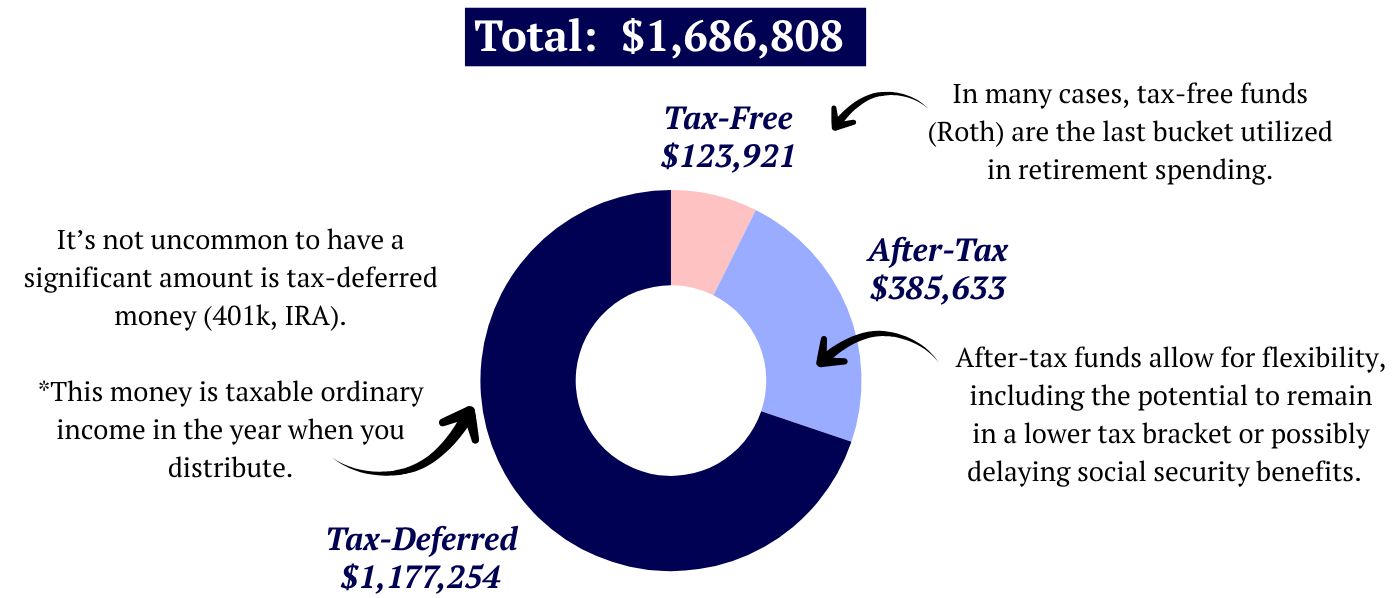

Add It Up: How much do you have in 401(k)s, IRAs, or taxable accounts? What about liquid savings? It's important to know the tax status of your dollars for efficient liquidation. Your investment accounts should fit into one of these categories:

Here's an example:

Calculate how long will it last. A good starting point is the 4% rule, which assumes you withdraw 4% of your portfolio balance each year. Research from Morningstar suggests that at this level, a portfolio can last 30+ years, making this a conservative assumption. For the sample portfolio above, the client can distribute $67,472/year based upon the 4% rule.

“When Can I Retire?” This question continues to plague investors, as many factors need to be considered. Analyzing your life expectancy, income sources, expenses, & your portfolio will get your off to a good start. For a decision of this magnitude, it's a good idea to consult with a professional to develop a plan. Surprisingly, according to a2024 Schwab survey, only 36% of Americans have a plan in place. However, of those who do have a plan, 96% of them feel confident about reaching their goals.

How We Plan: At Elite Wealth, we use a "Monte Carlo Analysis" to help determine if our clients are on track. The analysis is designed to model the uncertainty and variability of future outcomes by running 1,000 simulations of a retirement plan, producing a probability of success score (or lack thereof).

While the Monte Carlo Analysis isn't perfect, it’s a great starting point to help identify potential issues that are present with a client’s current financial picture.

What if....One thing we know is that the original plan won't play out perfectly. To combat this, we provide details on many "what if" scenarios to see how your plan would hold up, such as:

By modeling various "what if's" along with updating our client plans every 6 months, we strive to create a level of financial comfort that otherwise wouldn't exist. As a result, we frequently see clients becoming more comfortable with short-term market moves as their focus shifts towards the big-picture planning.

As an advisors who's built hundreds of plans, the biggest hurdle for most is simply getting started. With today's technology, it's never been easier to get your plan off the ground. While financial planning won't answer all of your questions, it will at least get you headed down the right path. Getting a handle on your own personal cashflow, tax rate, & investments will help you better understand how your future may ultimately unfold.

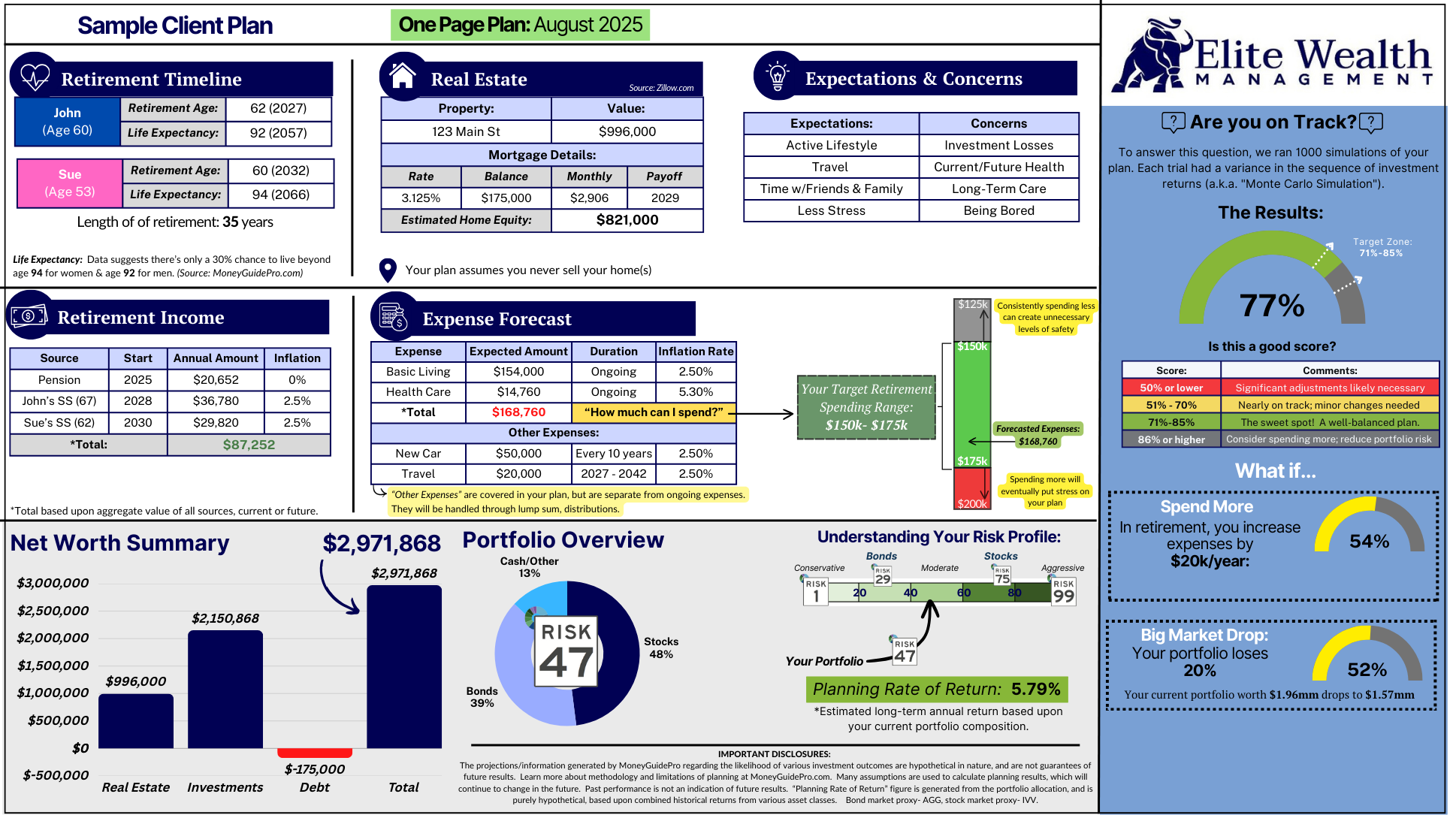

Ready to Get Started? Here's a sample of our One Page Plan:

Important Disclaimer: The information provided in this guide is for educational purposes only. All examples used are based upon a fictitious client that resembles our typical clients. Nothing here within should be considered investment or tax advice. Please consult with a financial advisor and/or CPA when considering investment and tax decisions.

We generally serve families with $500k or more in retirement/investment assets. Our clients are seeking a trusted advisor to oversee investment decisions and retirement planning. Schedule a meeting to explore our services:

Schedule a Call

.png)