If you've ever had this thought, you're not alone. And by now you should now how the world works, things never seem to settle down...

Markets are hovering near all-time highs. Economic headlines swing between optimism and concern. Many smart, successful people are sitting on cash — waiting for a “better” entry point or the next market dip. But here’s what the data actually shows: Right now — today, with the money you have available — is statistically one of the best times to invest for the long term. Charles Schwab studied this exact question. Their analysis reveals that the cost of waiting for the perfect moment almost always outweighs the benefit of even flawless market timing. And let's be real, perfect timing is impossible, so the smartest move for most long-term investors is to invest as soon as possible.

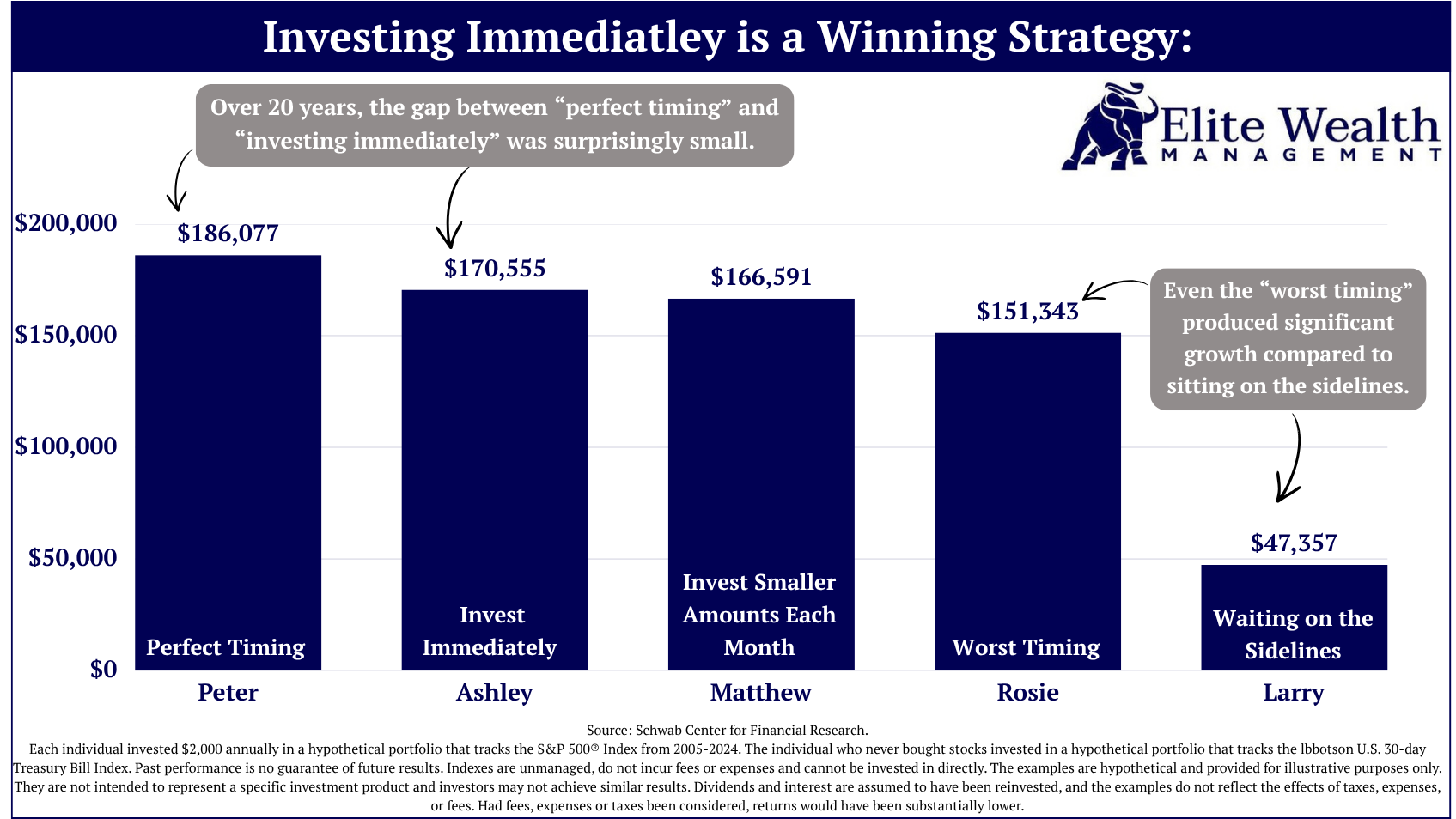

Schwab modeled five investors who each received $2,000 at the start of every year from 2005 through 2024; a grand total of $40k. They all had the ability to invest in the S&P 500, but used various methods/timing:

Meet Your Investors:

The results speak for themselves. After 20 years, here are the portfolio values for our 5 hypothetical investors:

The gap between perfect timing and simply investing immediately was surprisingly small. And what's even more telling-consistently bad timing beat sitting on the sidelines by a wide margin. Procrastination was the real portfolio-killer.

No! Schwab also reviewed 80 different 20-year rolling periods going back to 1926. The pattern held strongly: getting money into the market quickly consistently outperformed waiting.

Of course, stocks involve risk, and past performance doesn’t guarantee future results. But the data is clear: the longer your money stays on the sidelines, the more potential growth you leave behind.

Stop waiting for the “perfect” time. Right now is one of the best times to put your available money to work according to your long-term plan. Whether you invest it as a lump sum today or set up automatic monthly contributions, the most important step is getting started. The market’s long-term upward bias rewards participation far more than prediction. Create (or revisit) your investment plan, take action, stay diversified, and let time and compounding do the heavy lifting.

Ready to Get Started? Click here to invest with us.

Important Disclaimer: The information provided in this guide is for educational purposes only. Any examples used are based upon a fictitious client(s) that resembles our typical clients. Nothing here within should be considered investment or tax advice. Please consult with a financial advisor and/or CPA when considering investment and tax decisions. Based on Schwab’s analysis (updated July 2025). This is not personalized investment advice.

We generally serve families with $500k or more in retirement/investment assets. Our clients are seeking a trusted advisor to oversee investment decisions and retirement planning. Schedule a meeting to explore our services:

Schedule a Call

.png)